Construction Loan Myths That Cost Builders Time and Money

Most builders assume construction loan requirements follow the same rigid playbook as a traditional mortgage. That assumption stalls projects before ground is broken. Construction financing operates on entirely different mechanics. The gap between what builders believe and what lenders actually require costs weeks of approval time, thousands in holding costs, and opportunities that vanish while paperwork sits in underwriting.

The construction loan process isn’t complicated because lenders want it to be. It’s structured around risk mitigation during the construction phase, when your project exists only as plans and permits.

Understanding how construction loans work, what separates a construction-only loan from a construction-to-permanent loan, and why your debt-to-income ratio matters differently during the building project than it does for permanent financing changes how quickly you secure funding.

What follows are the most persistent myths about construction loan requirements, drawn from hundreds of funded projects. Each represents a specific bottleneck that slows builders. Each includes the actual requirement and how to address it before you submit your loan application.

Why Construction Financing Myths Persist

Most construction financing “rules” you’ve heard were written for homeowners building a single custom home, not professional builders running spec projects. Traditional banks established these requirements for owner-occupied home construction loans, treating them as a standard mortgage application. That’s a completely different animal than spec building, where you’re running a business and need financing that moves at market speed.

The problem is that consumer-focused content dominates search results. When you look up construction loan requirements, you often find advice intended for first-time homeowners, not experienced builders managing cash flow across multiple projects. Private lenders emerged specifically because traditional banks couldn’t effectively serve spec builders. Banks evaluate construction loans using the same underwriting standards they apply to conventional mortgages. That approach doesn’t account for your track record, your ability to manage subcontractors, or your understanding of local market timing.

Builder-focused lenders evaluate projects differently. They assess your experience, the strength of your proposal, and whether your timeline aligns with current market conditions. The myths persist because most builders learn financing rules from other builders, who learned from banks that never specialized in spec construction. You hear “you need 20% down” or “approval takes two months” enough times, and it becomes accepted wisdom. Meanwhile, lenders who actually understand ground-up projects are closing construction loans in 15 days with 10% down for builders with strong track records.

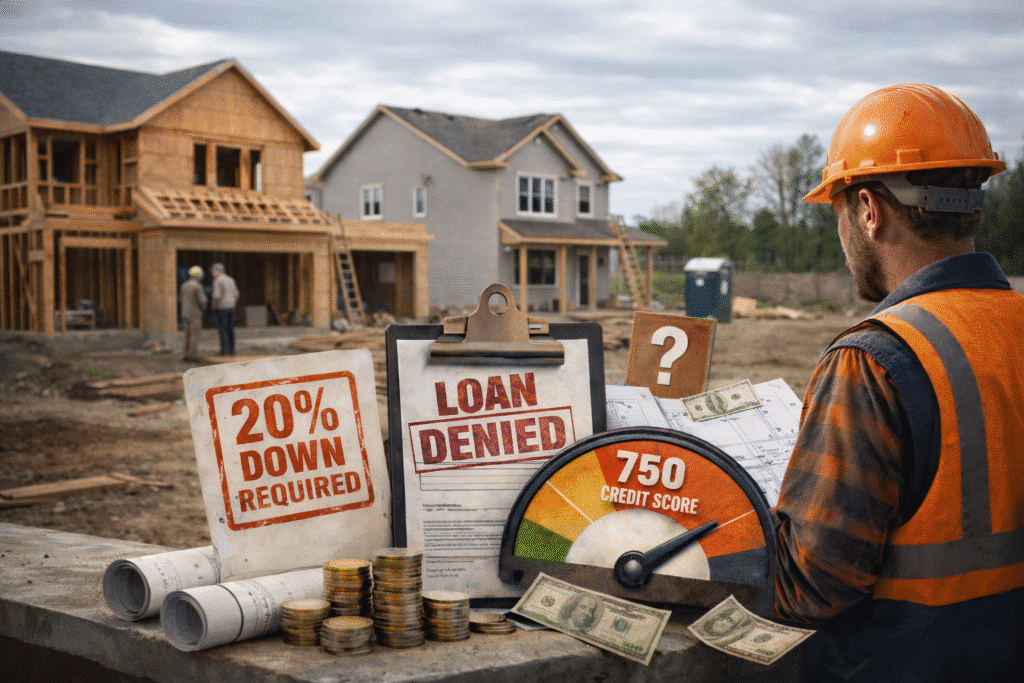

The Perfect Credit Score Myth

You’ve probably heard that you need a credit score of 700+ for a construction loan. That’s the standard for a traditional mortgage, and traditional banks apply those same requirements to construction loans because they use identical underwriting guidelines. But private lenders who specialize in builder financing use asset-based lending, where your project’s strength matters more than your personal credit history.

Builder-focused lenders have closed construction loans for builders with credit scores in the 580-620 range when project fundamentals were solid, and the builder had verifiable experience. Your credit score still matters, but it’s not the dealbreaker many assume. Asset-based underwriting focuses on project collateral, such as land equity and after-repair value. Some lenders approve construction loans for builders who’ve had past credit issues if the current deal is strong and you can demonstrate you’ve successfully completed similar projects since then.

Traditional banks can’t do this because their underwriting systems are built for consumer loan approval, not for evaluating the viability of construction projects. They require a score of 680+ because their systems flag anything below as high-risk, regardless of your building track record. The difference comes down to what the lender is really evaluating.

Banks look at your ability to make monthly payments like a homeowner applying for a traditional mortgage. Builder-focused construction lenders look at whether you can complete the project on time and on budget, then sell it for the projected price. Your last three projects matter more than a credit report ding from five years ago.

The 20-30% Down Payment Myth

Traditional banks state that you need 20-30% down payment for a construction loan. That’s true if you’re working with a bank, but it’s not a universal construction loan requirement. Private lenders routinely fund up to 90% loan-to-cost for builders with strong projects and track records. The key is understanding how different construction lenders calculate your required cash investment and what counts toward that down payment.

Lot equity changes the entire down payment calculation. If you own a permitted lot free and clear, most lenders will count up to 75% of that lot’s value toward your construction loan down payment requirement. On an 85% loan-to-cost deal, that lot equity might cover your entire cash requirement, meaning you break ground with minimal additional capital. Ground-up financing at 85% LTC is common, and 90% is available for strong deals and demonstrated experience.

Here’s the trade-off: lower down payments typically mean higher interest rates. A lender funding 90% of your construction costs is taking more risk than one funding 75%, so they price that difference into your rate. Run the numbers on how much working capital you preserve versus the additional interest cost.

Smart builders structure construction loan deals to preserve working capital. Understanding your true down payment options is the first step to keeping more cash in operations, where it generates returns rather than sitting idle as equity in a single project. This is one of the critical financing decisions that separates builders who scale from those who stay stuck.

What You Actually Pay During Construction

One question builders often overlook: What do you pay during a construction loan? Unlike a traditional mortgage, where you pay principal and interest from day one, most construction loans use interest-only payments during the construction phase. You pay interest only on the amount drawn, not on the full construction loan amount. This keeps your monthly payments lower while construction progresses.

For example, if you have a $500,000 construction loan at 10% interest but have drawn only $200,000 so far, your interest payments are calculated on the $200,000 drawn. As you pull more draws and construction progresses, your monthly payment increases. This structure helps manage cash flow during the construction phase, when you’re not yet generating income from the property. Construction loans cover your construction costs incrementally, rather than in a lump sum, as with permanent financing.

The construction period typically ranges from 6 to 12 months for a single-family spec home. During this period, you’re making interest-only payments in line with your draw schedule. When construction is complete, you either refinance into permanent financing, sell the property, or if you have a construction-to-permanent loan, the loan automatically converts to a permanent mortgage with principal and interest payments. Understanding this payment schedule upfront helps you budget accurately for each building project.

The Slow Approval Timeline Myth

Traditional banks typically require 60-90 days for construction loan approvals, while private construction lenders routinely close in 15-21 days. That 45-day difference isn’t just convenient. It’s the gap between securing a deal and watching a competitor break ground on the lot you wanted.

Banks move slowly because their documentation requirements are extensive and their underwriting committees meet on fixed schedules. Builder-focused construction lenders structure their operations around speed because they understand that every day a project sits idle costs you money. Same-day analysis and term sheets are standard from lenders who specialize in spec construction. You submit your project details in the morning and receive preliminary construction loan approval by afternoon.

The closing timeline depends on how quickly you provide documentation, not on waiting for committee meetings. Draw processing speed is as important as initial approval. Banks take 7-10 days to process draw requests. Private lenders focused on builders’ process draws in 48-72 hours because they know your subcontractors don’t wait two weeks for payment. Speed creates competitive advantage in hot markets.

When you can close a construction loan in three weeks instead of three months, you can move on to opportunities other builders miss. You can negotiate better pricing with sellers who need quick closings. Every day you wait for loan approval is a day your crews aren’t working and your competitors are breaking ground.

Understanding Different Types of Construction Loans

Not all construction loans work the same way. Knowing the types of construction loans available helps you match the right product to your project. A construction-only loan covers the construction phase and requires you to refinance into a permanent mortgage loan when construction is complete. This short-term loan works well for spec builders who plan to sell before needing permanent financing.

A construction-to-permanent loan combines both phases. Once construction is complete, the loan automatically converts to permanent financing without requiring a second closing or additional closing costs. This loan type makes sense for builders who might hold a property as a rental if it doesn’t sell immediately. You save on closing costs by avoiding two separate loan closings.

For builders doing renovation projects, a renovation loan covers both purchase and rehab costs. Similar to ground-up construction loans, draws are released as work is completed. Bridge loans serve a different purpose, helping builders manage transitions between projects or acquire property quickly while arranging longer-term financing.

Each loan type has different interest rates, terms, and requirements. Whether you need a short-term loan for a quick flip or a construction-to-permanent structure for a potential hold, the right choice depends on your exit strategy and timeline.

Stop Losing Deals to Outdated Rules

The construction loan requirements slowing you down weren’t designed for spec builders running multiple projects. They were created for homeowners financing a single residence and were later applied universally by traditional banks that never adapted to professional construction financing. Understanding this distinction changes everything.

Your credit score, down payment, approval timeline, and lender choice all operate under different rules when you work with builder-focused private construction lenders who evaluate project strength over consumer mortgage criteria. Every myth you’ve accepted as fact represents capital sitting idle, opportunities missed, and competitors gaining ground while you wait for outdated banking systems to catch up.

Builders closing construction loans in 15 days with 10% down aren’t receiving special treatment. They’re working with lenders who understand that spec construction demands speed, flexibility, and expertise that traditional mortgage underwriting simply cannot provide.

The construction loan obstacles you’ve been managing aren’t inevitable. They’re the product of working with institutions that never specialized in what you do. When you choose a construction lender with builder DNA, the rules change in your favor.